The 2022 Cloud 100 Benchmarks

Bessemer reveals insights into the 2022 Cloud 100 cohort—valuation marks aren’t always a true indicator of fundamental performance and Centaurs are dominating the private cloud market.

Originally published in Bessemer’s Atlas. Co-authored by Mary D’Onofrio, Janelle Teng, and Andrew Schmitt.

Today Bessemer Venture Partners, Forbes, and Salesforce Ventures announced the 2022 Cloud 100 List, the definitive ranking of the top 100 private cloud companies. Last year, the estimated valuation required to make the Cloud 100 list was over $1 billion, and the median was $3 billion. This was a record-high threshold for which—for the first time in history—each honoree had to achieve the unicorn milestone to be on the list.

This year, the bar has been set even higher. Not only have all of the 2022 Cloud 100 honorees again reached at least the $1 billion valuation milestone, but also the average Cloud 100 valuation has skyrocketed to $7.4 billion. The median is an impressive $4.6 billion.

But wait, aren’t the public markets in turmoil? With rising inflation, decreased stock prices, and the fears of recession looming, why did private cloud valuations continue to get bigger? We note that all of the 2022 Cloud 100 honorees raised their last private round between 2020 to early 2022, when the cloud market was far more exuberant than it is today. All of the companies on this years’ list raised before the downturn and are still holding on to these high private marks.

Given the ebullient market backdrop of 2020 and 2021, we recently wrote about the need to return to business metrics outside of valuation that cannot be so easily gamed, and we looked for a milestone rooted in business fundamentals. And the milestone that we celebrate now is reaching $100 million of ARR, which we call becoming a Centaur.

Based on this year’s data, over 70% of 2022 Cloud 100 companies are currently Centaurs, with an additional about 10% expected to hit this milestone by the end of the year—marking over 80% of 2022 Cloud 100 honorees as Centaurs! This is a primary reason why we have conviction that this year’s honorees truly represent the best cloud companies globally.

With seven years of Cloud 100 data behind us, in this year’s Benchmarks Report we reveal Bessemer’s analysis and insights into the 2022 Cloud 100 cohort and what it tells us about the Cloud Centaurs in the private cloud market today.

Top highlights:

Private cloud valuations continue to get bigger. The Cloud 100 2022 is worth an aggregate of $738 billion in 2022 vs. $518 billion in 2021, which is a 43% increase year-over-year and 7.5x increase since 2016. The top 10 Cloud 100 companies alone contribute $252 billion of equity value (34% of list value).

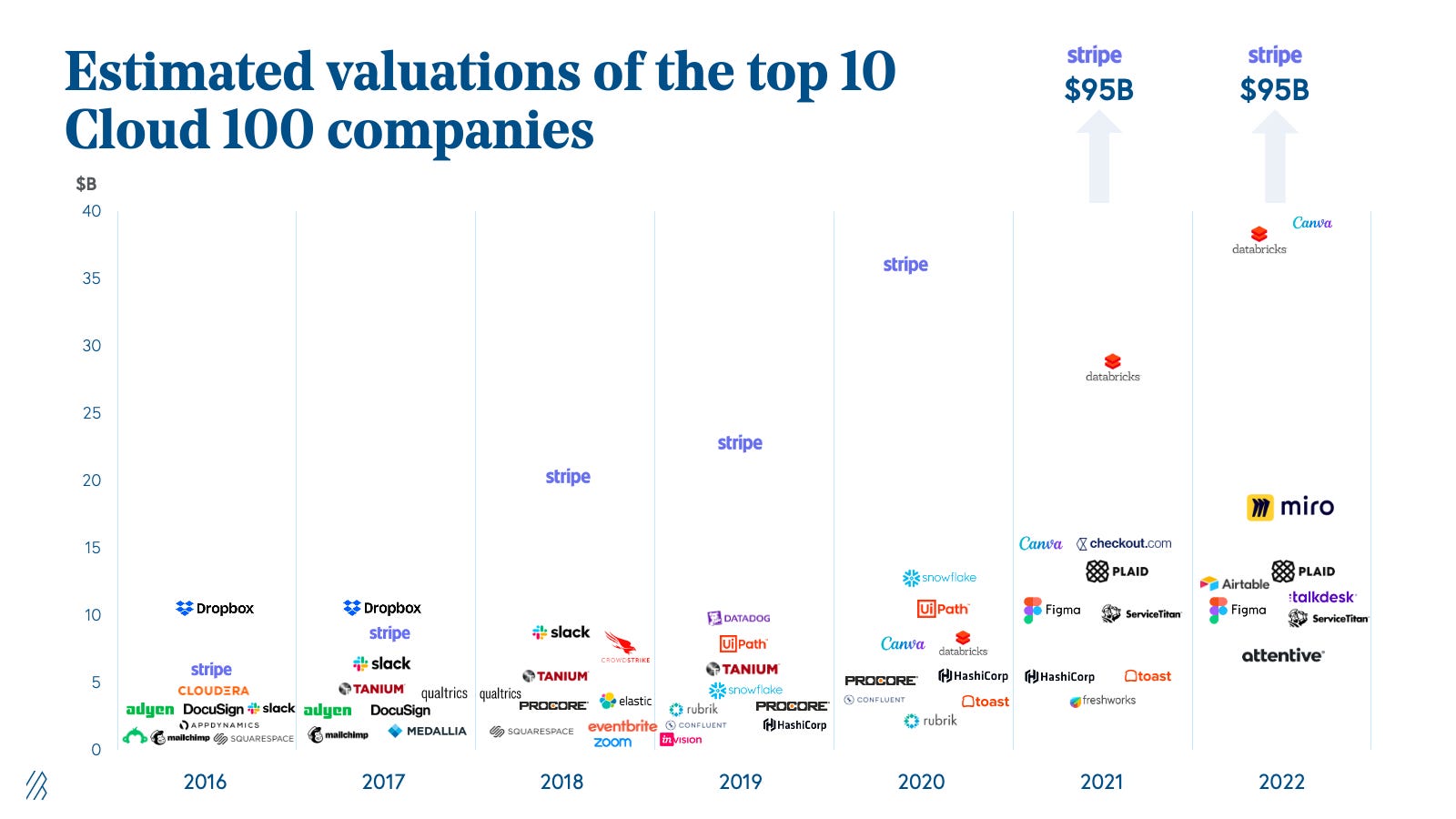

Similar to last year’s trend, Fintech represents the highest value subsector at $191 billion (26% of list value), anchored by Stripe that contributes $95 billion of market cap alone per its last private financing. This is followed by Design/Collaboration/Productivity at $116 billion (16% of list value), and data/infrastructure at $96 billion (13% of list value).

The threshold to make the Cloud 100 continues to get higher: similar to last year, every company on the list has at least hit the $1 billion+ valuation milestone. In addition, the average cloud company valuation was $7.4 billion, an increase of $2.2 billion year-over-year. Note, however, that all 2022 Cloud 100 companies raised prior to early 2022, keeping their high marks they earned pre-downturn.

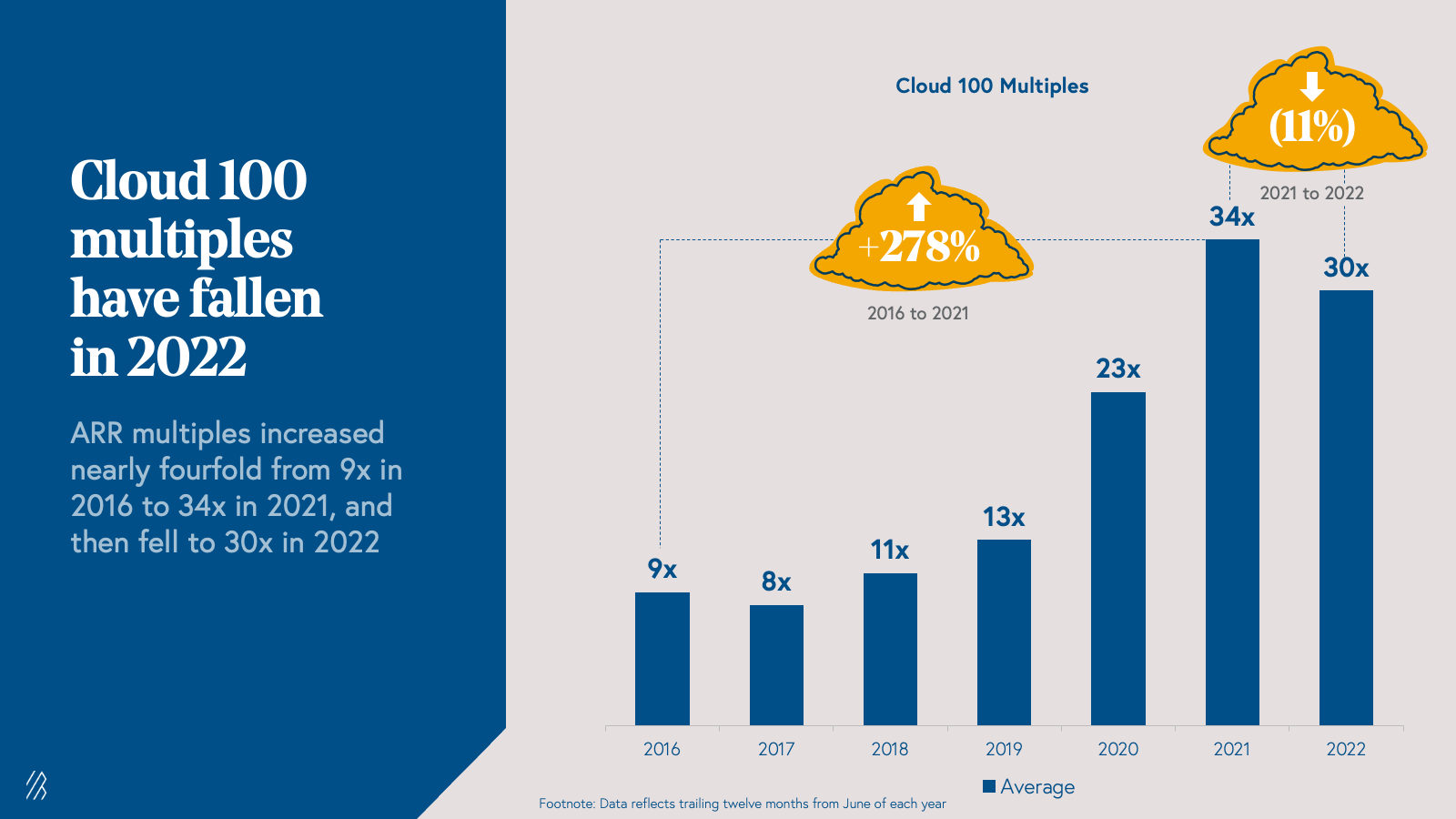

Something notable this year is that as the public markets began to cool, the average Cloud 100 multiple has decreased slightly from 34x in 2021 to 30x ARR, though the average growth rate actually increased to 100% year-over-year.

Given the fact that valuation can be an illusion, at Bessemer we choose to use a more reflective metric: the Centaur milestone of achieving $100 million of ARR. We are proud to observe that over 70% of 2022 Cloud 100 Honorees are currently Centaurs, with an additional about 10% expected to hit this milestone by the end of the year—marking over 80% of 2022 Cloud 100 honorees being Centaurs. Impressively, it took an average of eight years from their founding for Cloud 100 Centaurs to hit this milestone.

It is no surprise that since these are the best-in-class companies as defined by fundamental performance rather than arbitrary valuation marks, the Cloud 100 list continues to produce strong returns. In seven years, the total valuation of the 2016 Cloud 100 list has increased by more than $469 billion, delivering a 5.8x and 34% IRR in that time. The 2017 Cloud 100 basket has delivered an 6.3x and 45% IRR as its aggregate value nears $735 billion; the 2018 basket a 4.8x and 48% IRR; the 2019 basket a 3.8x and 55% IRR; the 2020 basket a 2.6x and 62% IRR, and the 2021 basket a 1.4x and 37% IRR in just one year alone.

The 2022 Cloud 100 at a glance: $738 billion of equity value

The 2022 Cloud 100 list represents an astonishing $738 billion of equity value, with an average $7.4 billion valuation per company. The cumulative value of the Cloud 100 list is up a staggering +43% from the 2021 list’s aggregate value of $518 billion, in just one year.

This valuation growth was catalyzed in part by both a high-priced multiple environment and the sheer volume of capital that went into cloud businesses: $129 billion in 2021 per Pitchbook. In many ways, it may have been wise of these companies to take advantage of market conditions to reduce dilution and buffer their cash runway in anticipation of more challenging times ahead.

This year we welcomed 25 new companies to the Cloud 100 list. The highest-ranked new entrant was Algolia, which graced the Cloud 100 list in 2018 and returns in 2022. Other newcomers include Clickup and Dataiku, alongside Bessemer portfolio companies Hibob, the modern HR platform; Alloy, the identity decisioning engine for financial services; and Netlify, the web development and deployment platform.

This year’s biggest mover title goes to Grafana Labs, the performance monitoring platform, which moved up +43 spots to #37 on the Cloud 100 list and announced its Series D raise at a $6 billion valuation in April.

The Top 10 Cloud Companies represent over $252 billion of equity value alone. Stripe retains the #1 spot on the Cloud 100 for the second year in a row (and fifth year overall) with its last private financing at a $95 billion valuation. Joining Stripe in the top ten are Databricks (#2), Canva (#3), Miro (#4), Figma (#5), Airtable (#6), ServiceTitan (#7), TalkDesk (#8), Plaid (#9), and Attentive (#10). At #4, Miro had the largest jump of any Top 10 company, increasing +32 spots from its #36 position on the 2021 list.

Representing $252 billion as a group, the Top 10 Cloud 100 companies individually average a valuation of $25.2 billion, which is up +$5 billion from 2021 and +$22 billion from the inaugural 2016 list. Some notable financings in this group include Canva’s September 2021 round at $40 billion and Miro’s December 2021 round at $17.5 billion. The strength of the Top 10 companies cannot be overstated; from the 2021 list Toast, HashiCorp, and Freshworks all successfully went public in the second half of 2021. We anticipate that the most anticipated cloud IPOs in the future (when the IPO window opens!) will be from this Top 10 list.

Digging into sub-sectors, Fintech continues to represent the most valuable Cloud 100 category at $191 billion (and 26% of total list value), though that market cap is anchored by Stripe’s $95 billion valuation in the last round. The next most valuable category is Design/Collaboration/Productivity, which contributes 16% of list value with $116 billion of market cap. Cloud 100 winners from this category include Figma, Airtable, and Notion. Data/Infrastructure rounds out the top three with $96 billion of market cap and 13% of list value, inclusive of companies like Databricks, Scale AI, and Fivetran.

While Fintech is the most valuable category by market cap, the highest number Cloud 100 honorees come from the Sales, Marketing, and Customer Success category. With 16 companies represented including Attentive, Klaviyo, Yotpo, and Intercom, it retains its top spot on having the most number of Cloud 100 honorees year-over-year.

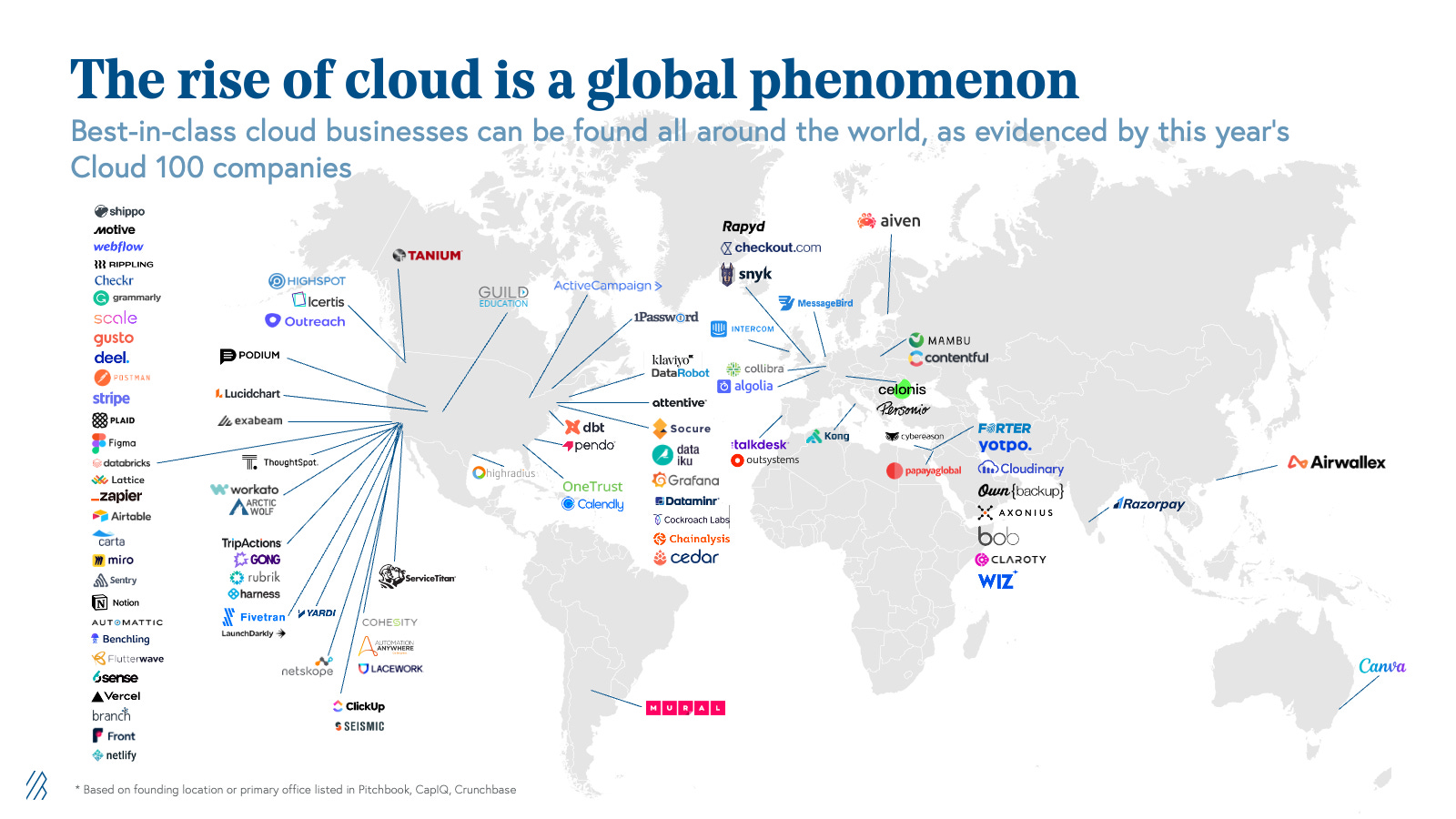

We noted last year that as entrepreneurs, operators, and investors all around the world increasingly recognize the power of the cloud, we’re seeing cloud startups bloom in technology hubs globally. Building on our prediction from last year, international representation on the 2022 Cloud 100 list has now surpassed 30%. In State of the Cloud 2022, we noted that public cloud spend is only 10% of the total $4 trillion total IT spend across the globe, with lots of untapped potential in regions such as Europe, Latin America, and Asia-Pacific. Using public cloud spend as a leading indicator of spend on all SaaS, we expect the Cloud 100 to become more and more geographically diverse in the coming years, as the globalization of cloud continues.

Valuations can be misleading, but Centaur status is a clear measure of traction

As we discussed above, the 2022 Cloud 100 list is worth an aggregate of $738 billion, an impressive +43% year-over-year growth over the $518 billion value of the 2021 list, increasing the average Cloud 100 winner’s valuation up to a massive $7.4 billion year-over-year ($6.5 billion if you remove Stripe). This must be surprising given the backdrop of deteriorating public markets, but as we noted, all of the 2022 Cloud 100 honorees raised their latest round in peak conditions before the downturn, and are still holding on to these high private marks.

However, we observe this year that as the market begins to cool, the average Cloud 100 multiple has decreased slightly from 34x in 2021 to 30x, reinforcing the frenzy of 2021 in the private cloud markets. Considering that the average public BVP Cloud Index company is trading under 10x, we expect that private multiples will continue to compress, though it may take several more quarters.

But while fears of recession, decreased purchasing power, and forecasted longer sales cycles are being often talked about in cloud company board rooms, thus far the performance of Cloud 100 companies continues to defy gravity. Even with these widespread macro concerns, the average Cloud 100 revenue growth rate actually increased to 100% year-over-year, with some companies forecasting even 200% or 300% growth for 2022. Taken in combination with the decreased multiples, growth-adjusted multiples improved year-over-year and returned to 2020 levels.

While we continue to celebrate the fundraising milestones of Cloud 100 companies, and the minimum threshold for this year’s list was $1 billion, we note that valuations are not always reflective of a company’s fundamental value when capital is easily accessible and markets are frothy. A decade ago, reaching the $1 billion valuation milestone was an exceptional accomplishment and a genuine proxy for success that signaled to customers, partners, employees and the media that a company should be taken seriously because it would likely endure. At that time, only 14 private startups were valued at $1 billion or more at the time, and only four unicorns were added to the herd yearly. However, as multiples increased and many cloud companies saw successful IPOs in a strong macro backdrop, capital flooded the cloud software startup ecosystem, driving the number of cloud unicorns to over 400+.

At Bessemer, this is why we choose to orient our companies, the broader VC community, and even ourselves, towards the more reflective company milestone of becoming a Centaur, a $100 million ARR business.

We are exceptionally proud to observe that over 70% of 2022 Cloud 100 Honorees are currently Centaurs, with an additional about 10% expected to hit this milestone by the end of the year—marking over 80% of 2022 Cloud 100 honorees as Centaurs! This year’s honorees possess an incredible ability to grow quickly at $100 million+ ARR scale, strengthening our conviction that this list truly represents the best cloud companies globally.

Impressively, it only took an average of eight years from the founding for Cloud 100 Centaurs to hit this milestone. On a category basis, the Sales/Marketing/CX category has the most Centaurs.

We congratulate every Cloud 100 company that has reached this exceptional milestone, including a very special Bessemer portfolio company that is proud to announce its Centaur status today—LaunchDarkly!

Cloud 100 returns: +477% increase in valuation since 2016

As highlighted by the high representation of Cloud Centaurs in the Cloud 100, these are best-in-class cloud companies as defined by fundamental performance rather than arbitrary valuation marks. It is thus no surprise that the Cloud 100 list continues to produce strong returns. In seven years, the total valuation of the 2016 Cloud 100 list has increased by more than $469 billion, delivering a 5.8x and 34% IRR in that time. The 2017 Cloud 100 basket has delivered an 6.3x and 45% IRR as its aggregate value nears $735 billion; the 2018 basket a 4.8x and 48% IRR; the 2019 basket a 3.8x and 55% IRR; the 2020 basket a 2.6x and 62% IRR, and the 2021 basket a 1.4x and 37% IRR in just one year alone.

While there were 11 IPOs/direct listings from the 2021 Cloud 100 members, the IPO window remained shut in 2022 given the market turning for the worse. In fact, several honorees had to postpone IPO plans for this year. Despite this, we still have conviction that Cloud 100 honorees are going to be the strongest IPO candidates when the window opens and perhaps targets of strategic M&A.

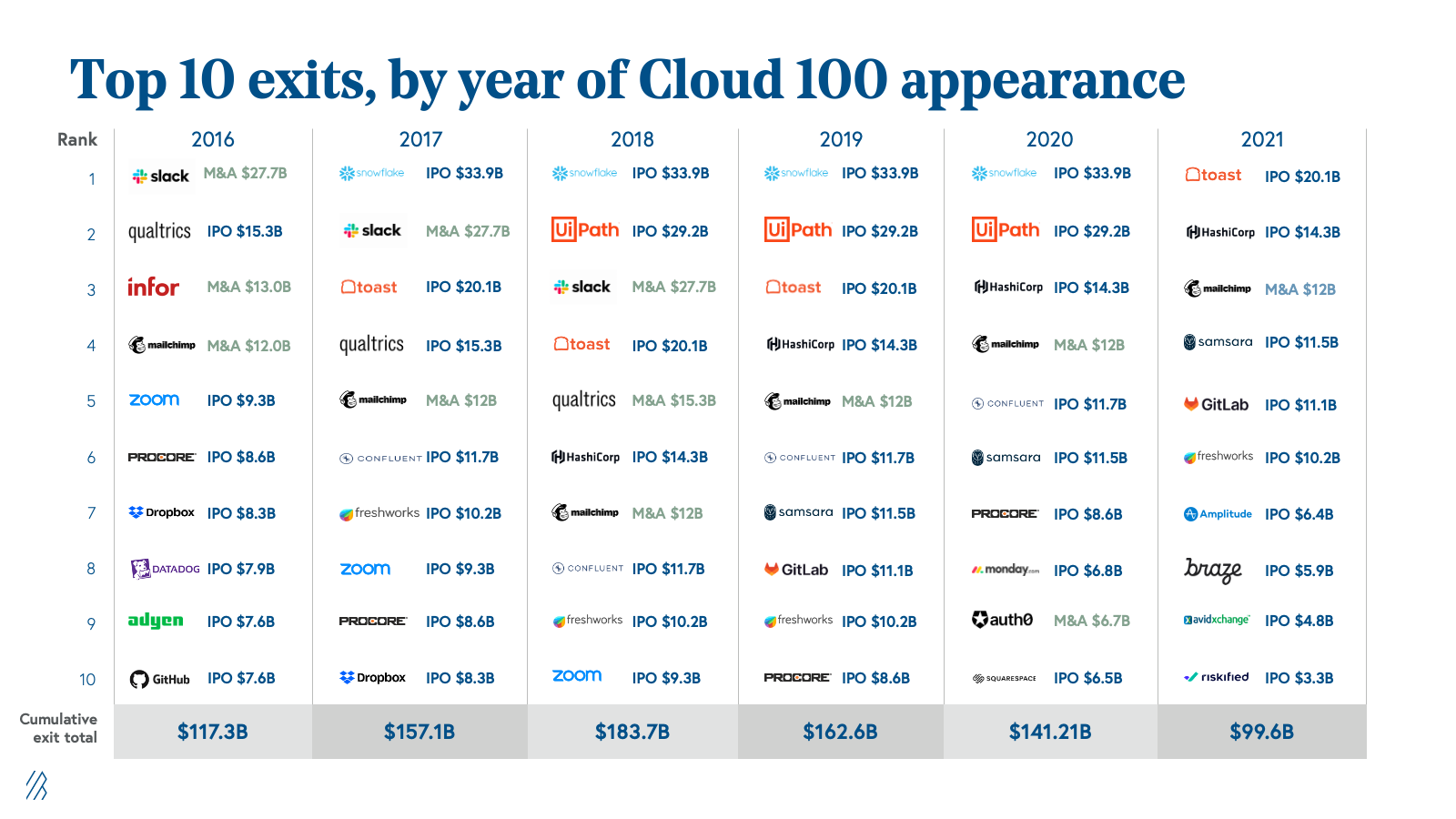

To highlight this potential, we reviewed exits per list year and found that the average exit size of Cloud 100 companies has been increasing over time, from an average of $3.3 billion in 2016 to $8.6 billion from realized exits in 2021. Historically, a majority of the exit value has been generated from IPOs, signaling how Cloud 100 members can grow into strong, standalone companies.

To illustrate this point, we note that iconic companies have IPOed from the Cloud 100 list, including the likes of Snowflake, UiPath, and Toast with their mega IPOs.

Focusing on strong business fundamentals

As we celebrate the 2022 Cloud 100 season, we want to remind entrepreneurs and investors that despite compressing multiples and what feels like doom-and-gloom in the markets, cloud businesses today are still displaying strong fundamentals.

As previous Cloud 100 graduates have demonstrated, the best cloud leaders are not only able to survive, but also thrive, through challenging times. These businesses are riding multi-decade tailwinds, and here at Bessemer we’re long-term oriented and long-term bullish on these companies. From the high percentage of Centaur representation in the 2022 Cloud 100 cohort, these honorees have already proven that they are companies with strong, durable fundamentals which gives us great conviction that the world’s best cloud companies will be able to weather the storm.

See you for the 2023 Cloud 100!

Read more Centaur Studies from ServiceTitan, Calendly, and LaunchDarkly in The Centaur Report.