SaaS: Have reports of my death been greatly exaggerated?

Sentiment is brewing in the public and private markets that it's the end of SaaS. Is a mass extinction event really imminent for the industry?

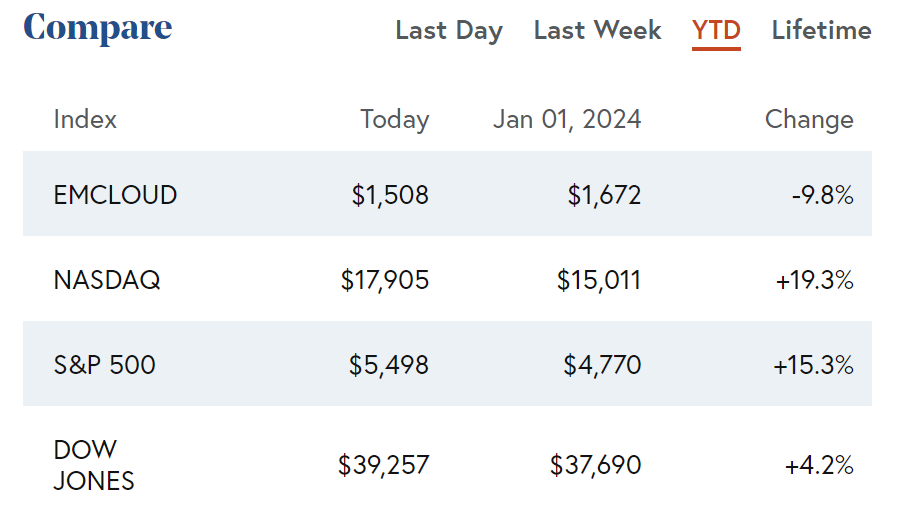

No sugar-coating here: 2024 has not been kind to SaaS companies. The latest earnings season for public SaaS companies just wrapped up, and outlook remains muted as results revealed another weak quarter for the cohort. SaaS, especially small cap, has meaningfully underperformed broader market indices year to date:

As I had written earlier in the year, while it’s clear that an era of hypergrowth is over for the industry, fundamentals and demand signals for public SaaS companies continue to show a deteriorating trend and are at some of the lowest levels in recent years:

Looking at performance of the cohort relative to consensus expectations, signals around beat cadence have been inflecting negatively and are now below trailing 4-quarter and 8-quarter trends:

As a consequence, in a notable reversal from prior quarters, a significant majority of SaaS companies faced negative share price reaction post earnings this quarter (chart below) and some SaaS bellwethers even experienced their worst one-day stock price decline in two decades.

Is it the end of SaaS?

These public market data points are feeding a pessimism within the private markets that SaaS is dying. A memo from Chris Paik of Pace Capital went viral in the VC world recently, asserting that it’s “The End of Software”. Underpinning this narrative is sentiment that AI will be a swift disruptive force to the SaaS industry across many vectors — from distributing control over a wider set of companies, to catalyzing a shift toward AI-powered services and vertical specific AI-enabled work, to inverting unit economics for the application layer:

At the surface, it does seem somewhat impetuous from the VC community to simply declare that an entire industry worth over $500bn (chart below) will be disrupted overnight.

Is a mass extinction event really imminent? Mark Twain once said that “the reports of my death have been greatly exaggerated”. So too do I view the news that SaaS is dead to be somewhat overblown at this point, since it’s probably more of a rebirth than true demise of the industry. Many incumbent SaaS players are undoubtedly very vulnerable from an existential perspective given the threat of AI. But just as in the natural world, the main factor drawing the line between extinction and evolution is time (I’m finally putting my biology degree to good use here!). You’ll notice that many of the articles asserting that it’s the end of SaaS do not have a timeline associated with their claims. Herein lies the key nuance for me — WHEN will AI-native solutions get good enough to replace traditional SaaS?

Currently, while it is easy to spin up a proof-of-concept as enterprises are willing and eager to experiment with AI, many AI deployments do not seem to be able to graduate beyond this stage, or tend to be limited to small scale projects for internal use cases. The real proof in the pudding will be at-scale AI deployments in-production, and the reality is that we may not be close to this end state yet:

From my interviews with hundreds of enterprise customers, graduation drop-off often arises due to a lack of reliability for business use cases, both in terms of AI unable to complete the steps of a task successfully, but also because the AI-powered solution may not offer a higher degree of accuracy compared to existing status quo options. Many AI applications do not yet display enterprise-grade reliability, or still require significant human-in-the-loop quality checks for the final output. The current conclusion is that the stakes are too high, especially in industries such as financial services or healthcare, to implement fully autonomous customer-facing AI solutions that could potentially hallucinate at unacceptable levels or just fail to complete tasks consistently.

This is understandable since we’re in such early innings of the AI wave, and I believe we’ll see a step-function change in real-world enterprise reliability within the next 18-24 months. Underpinning my enthusiasm are a a multitude of variables that I’ve written about previously, including:

unprecedented pace of innovation from a wide set of stakeholders including open-source contributors and academics/researchers

a blossoming AI Infrastructure ecosystem enabling developers to build more reliable AI applications

new AI model architectures that inherently exhibit lower hallucination levels

Software is constantly evolving

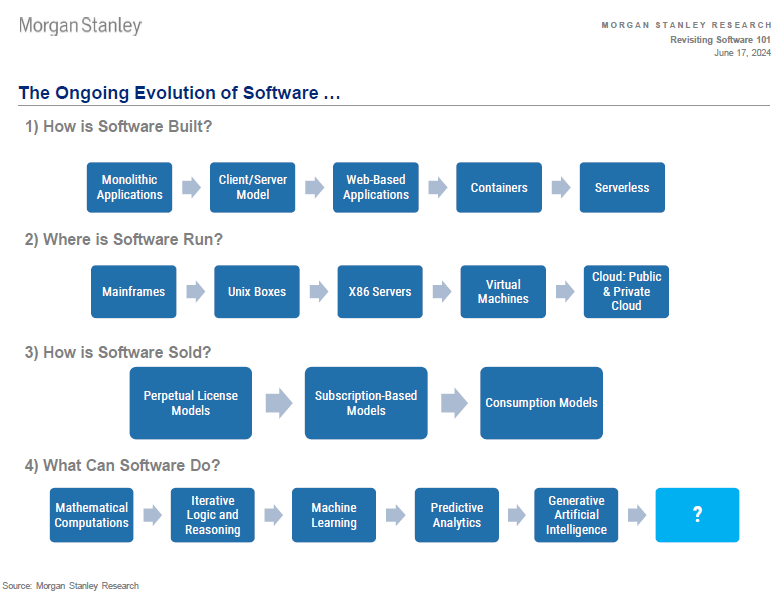

While historical precedent is not a guarantee of the future, the software industry is resilient and has gone through various evolutions over time, not just in terms of functionality and capabilities, but also across aspects of how software is built, where it is run, and how it is sold:

During the next few months, as AI grows in reliability to fulfill its eventual promise, traditional SaaS vendors have an opportunity to embrace AI functionality as the industry experiences a rebirth, or remain stagnant at their own peril. In fact, in our recently published State of the Cloud 2024, my colleagues and I at Bessemer went on record to assert that “The Legacy Cloud is dead – Long Live AI Cloud” as AI will push cloud businesses toward a new future. This opportunity will also be a challenge given the innovators’ dilemma, but this luxury of time should not be squandered by SaaS incumbents.

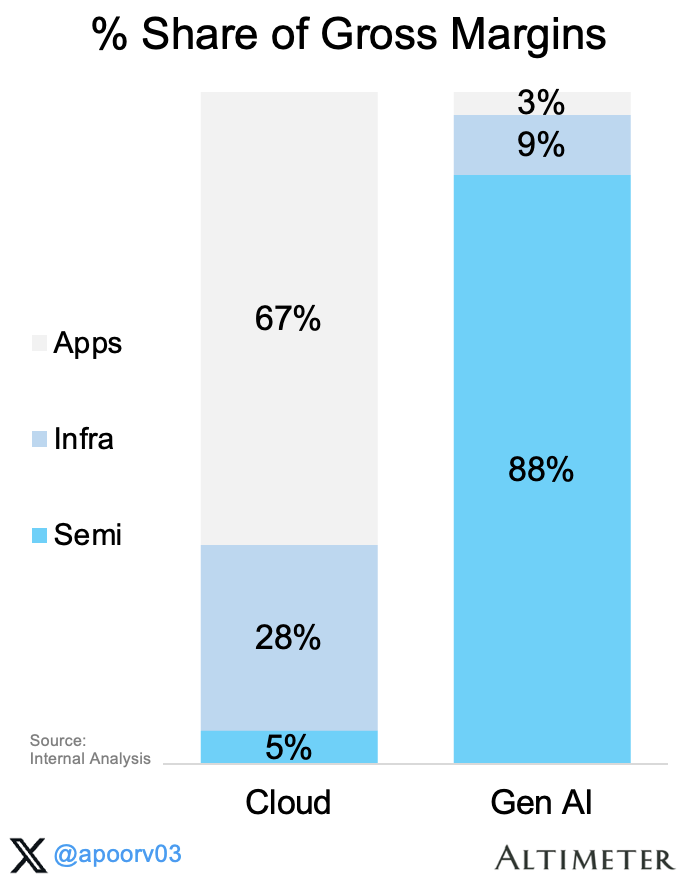

On top of new capabilities and product innovation, SaaS incumbents will need to consider creative approaches to pricing and packaging, especially as business models evolve beyond traditional seat-based subscription in the age of AI. As my colleagues and I pointed out in our State of the Cloud report, the introduction of new business models such as agents, co-pilots, and AI-enabled services (chart above) will likely spark new thinking around task-based pricing based on service spend/value, workflow volume, etc. Jamin Ball from Altimeter also wrote a thoughtful article recently articulating similar sentiment around the death of seat-based pricing since “the future of application software in a world of AI agents probably looks a whole lot more like database software”. Infra and developer-oriented software companies had already been moving in the direction of consumption-based pricing, but the AI apocalypse may just be the needed catalyst for SaaS apps to transition as we enter a new world of evolved software businesses.

Very interesting!

I think it's certainly on the end of SaaS, as you've hinted. But maybe we're going to have new buzzwords and acronyms to separate the different types of "SaaS" we're going to see in the future. Everything is going to be run on the cloud and offered online as "software", but different kinds of software: chatbots, automations, helpers/assistants for many verticals and more.

Very interesting article, thank you.

I am currently researching exactly this topic about the disruptive impact of AI on SaaS and this was quite helpful.